Table of Contents

- Executive Summary

- Reservoir Media Intro & Set-Up

- Reservoir Media Company Origin & Business Overview

- Historical Growth Driver: Acquisitions of Music Catalogues

- Functioning of the Business Model and Typical Revenue Streams

- Case Study: How to Add Value through Synchronization

- Current Owner Earnings of RSVR

- The Value Creation Engine

- Putting it all together: Valuation & Intrinsic Value Discussion

- Risks & Threats

- Conclusion, Catalysts & Portfolio Decision

Executive Summary

Based on current industry tailwinds (7%+ structural growth), prior experience with acquiring music catalogs, and the substantial gap between current valuation and realized transaction multiples (~8x vs. 14x NPS/NLS), we believe a double-digit return over the next 3-5 years is entirely possible by owning Reservoir Media.

During that timeframe, a potential catalyst could be a takeover offer from either a strategic buyer (a larger competitor like UMG, WMG, or Sony) or a PE fund aiming to further consolidate the market.

Apart from that, we believe that the continued growth of royalty income will, by itself, lead to a rising share price. Management around Golnar Khosrowshahi has a ~15-year track record of building and growing the company at attractive rates (with sufficient skin in the game and a long-term mindset).

Threats from AI seem unjustified given the proprietary nature of master recordings and publishing rights. Negotiating licensing fees for using song snippets, text passages, etc., in AI productions just seems to be the next step in the music industry’s “monetization” journey of the past decade. In the end, it takes a lot o

However, for the optimistic scenario to materialize (return >20% pa), a couple of things need to go right in the medium-term future:

- Growth of streaming platforms needs to materialize; the DSPs need to introduce a differentiated product offering (addressing the “superfan” demand), and continue raising prices regularly (ideally above inflation rate)

- Attractively priced M&A deals need to be available for the foreseeable future

- RSVR’s team needs to continue adding value to the portfolio through landing movie, TV, commercial, gaming, etc. placements (see the “synch” growth case study above)

We’d thus be willing to allocate 5-10% of our total portfolio assets to music royalties and believe RSVR is one of the best opportunities currently available. At ~7.6 USD/share, the stock looks promising.

To enter the position, we first allocate ~50% of the target 5%.

Reservoir Media Intro & Set-Up

We came across Reservoir Media (RSVR) while analyzing the much larger Universal Music Group (UMG), which is a key holding of Bill Ackman’s Pershing Square Holding.

As the Reservoir stock has not performed well over the past couple of years (basically moving sideways since its IPO in 2021), we thought it might be an interesting opportunity, especially given the asset-light and potentially very attractive business model of the two main operating segments.

Reservoir Media Company Origin & Business Overview

Reservoir Media (RSVR) is a US music company incorporated in Delaware and headquartered in New York City. The company was founded in 2007 by Golnar Khosrowshahi (a pianist by training) to build a portfolio of publishing rights and operate a royalty business (a model she had previously observed in the pharmaceuticals industry).

After growing the company for ~14 years in private, Reservoir was listed on the NASDAQ in 2021.

Compared to the „Big 3“ music companies (Universal Music Group, Sony Music Entertainment, and Warner Music Group), Reservoir can be considered a small-cap. As such, it is not followed very closely by Wall Street.

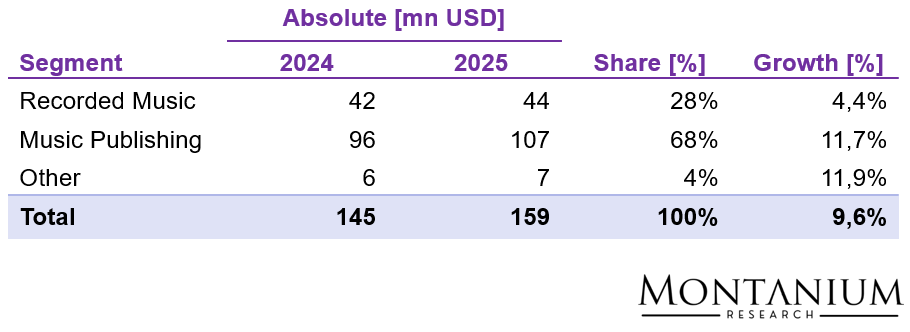

In 2025 (fiscal year ended on March 31), the company posted a revenue of USD 159 million.

Today, Reservoir basically operates two different business segments/has two main revenue streams:

- Music Publishing (~70% of revenue): Performance revenue, synchronization revenue, digital revenue, mechanical revenue, other revenue

- Recorded Music (record labels, ~30% of revenue): Subscriptions and streaming revenues, downloads and other digital revenue, physical revenue (vinyl, CDs, etc.), license and other revenue (e.g., when master recordings are used in movies, video games, or live shows)

Since 2019, Reservoir Media has managed to increase revenues by ~23% pa, which is quite an attractive rate:

![Figure 1: Revenue development Reservoir Media [USD million]; Source: TIKR, Reservoir reporting](https://montaniumresearch.com/wp-content/uploads/2026/02/RSVR-2-3-1024x466.png)

Figure 1: Revenue development Reservoir Media [USD million]; Source: TIKR, Reservoir reporting

As of the end of FY 2025, the Music Publishing segment was the largest segment, accounting for ~70% of total revenue:

Figure 2: Revenue breakdown Reservoir Media; Source: RSVR reporting

Compared to the longer-term growth rate of ~23%, growth has come down substantially, to ~9.6% in 2025.

Reservoir Media has historically been a US-centric company. Even today, the US remains the company’s largest revenue source, accounting for ~55-60% of sales in 2025. However, the Middle East (PopArabia), South America, and, most recently, India (PopIndia) are now key growth areas for the company.

![Figure 3: Sales Reservoir Media 2025 by segment and main geography [%]; Source: Company reports](https://montaniumresearch.com/wp-content/uploads/2026/02/RSVR-2-5-1024x461.png)

Figure 3: Sales 2025 by segment and main geography [%]; Source: Company reports

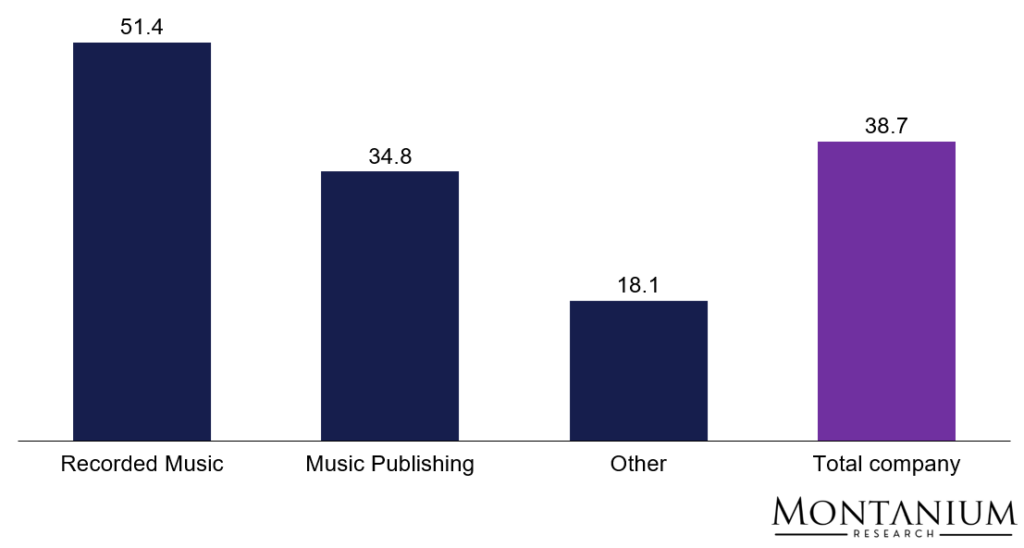

In terms of profitability, the Music Publishing and Recorded Music segments both exhibit an attractive margin profile with EBITDA margins comfortably above 30%:

Figure 4: EBITDA margins by segment [%]; Source: Company reports

Investors who know the music industry will immediately recognize that Reservoir’s EBITDA margins are substantially higher than those of the much larger competitors (e.g., UMG typically earns EBITDA margins of ~25%). This difference is largely due to Reservoir having a much smaller record-label business and thus much lower artist costs (an item that, for UMG, accounts for ~45% of revenue).

Historical Growth Driver: Acquisitions of Music Catalogues

For Reservoir Media, historically, growth to a large extent has been driven by M&A, more specifically, acquisitions of either music catalogs (publishing rights) from artists or other media companies, or of indie record labels, including master recordings and artist contracts.

Like PE-backed investment funds like the Hipgnosis Song Fund (now Recognition Music Group), Reservoir Media can be considered a so-called catalog consolidator.

However, takeover doesn’t necessarily equal takeover, and M&A transactions can typically be segmented by size. A company like Reservoir Media, seeking deals in the USD 1-50 million range, will mainly face competition from specialized investment funds (mainly PE funds) or other indie labels/music companies, but not so much from one of the 3 majors (for those, such small deals wouldn’t really move the needle).

A second major value driver has been the active increase in synchronization (“synch”) revenues by placing Reservoir songs in TV shows, movies, games, etc.

But how does the business model work anyway?

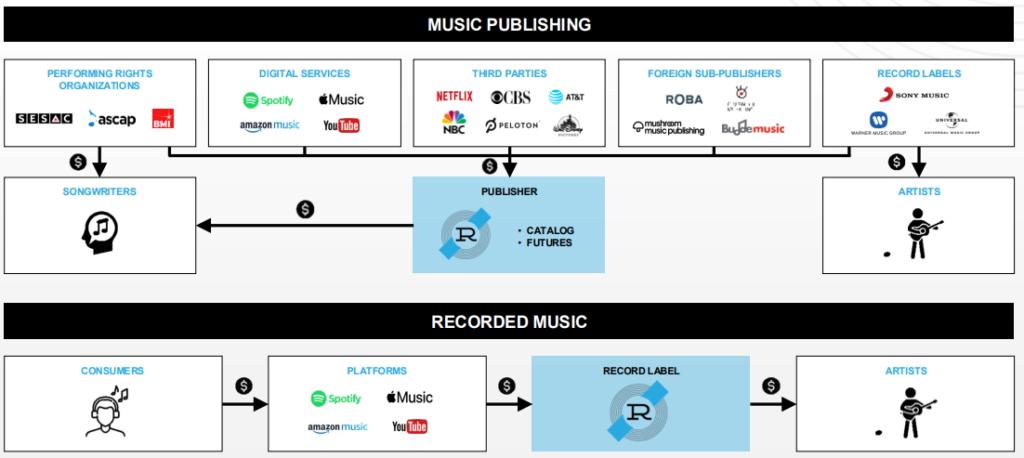

Functioning of the Business Model and Typical Revenue Streams

Reservoir Media’s two main businesses revolve around Music Publishing and Recorded Music. So let’s take a quick look at how money is actually made in these businesses (and the music business in general).

Music companies like Universal Music, Warner Music, or Reservoir Media typically have some or all of the following revenue streams/business segments:

- Recorded Music (record labels)

- Music Publishing

- Merchandising

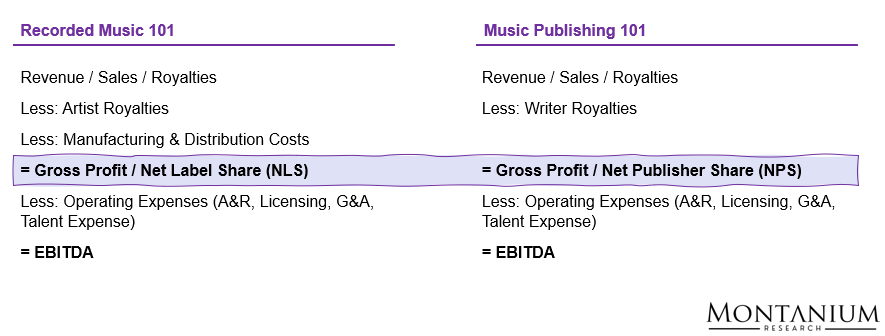

To make the distinction: generally, there are two types of music rights: (1) the master recordings and (2) the publishing rights.

Master recordings are the original recording files that get streamed and are sold as vinyl records or CDs (and revenues land in the Recorded Music segment), while publishing rights are royalties paid to the songwriters & producers who ‘publish’ a song and get paid when, for example, the song is played on radio or when other artists release covers of the song (recorded in the Music Publishing segment).

Here’s conceptually how those three businesses work:

Recorded Music (Master Recordings)

Recorded Music earns money by owning or controlling master recordings, which are typically licensed from artists under exclusive recording contracts lasting multiple albums over several years.

Streaming platforms (such as Spotify, Apple Music, YouTube, Amazon, Tencent) pay labels roughly 65-70% of their music-related revenue, which is then allocated to rights holders based on streaming share.

Contracts between label and artist are freely negotiated. However, the record label typically receives ~55% of the total distribution on average. Thus, the music company retains the majority of master revenue after paying artist royalties, marketing costs, and recouping advances, creating high operating leverage once a recording is successful.

In most traditional label deals, the record label (i.e., RSVR in this case) keeps the masters permanently, and the revenue share continues for as long as the recordings earn money – even after the artist contract has ended (a famous exception: Taylor Swift rerecorded all her old albums to obtain the rights to her masters).

As a result, the Recorded Music segment is highly attractive and displays substantial operating leverage.

Recorded Music revenues are derived from four main sources:

- Digital: the rightsholder receives revenues with respect to streaming and download services;

- Physical: the rightsholder receives revenues with respect to sales of physical products such as vinyl, CDs, and DVDs;

- Neighboring Rights: the rightsholder receives royalties if sound recordings are performed publicly through broadcast of music on television, radio, and cable, and in public spaces such as shops, workplaces, restaurants, bars, and clubs;

- Synchronization (“synch”): the rightsholder receives royalties or fees for the right to use sound recordings in combination with visual images, such as in films or television programs, television commercials, and video games.

Figure 5: Music 101; Source: Reservoir Media

Music Publishing (Compositions)

Music Publishing earns money by administering and monetising songwriting copyrights, which typically last 70 years after the songwriter’s death (after that, the composition becomes public domain). Therefore, the copyright expiry risk for compositions is extremely long-dated and basically irrelevant to our typical valuation horizon of a decade at most.

Composer and lyricist – if different people – are treated as co-authors of the composition, typically owning 50% of the composition rights each (but splits can vary).

For music companies like UMG or Reservoir Media, there are two monetization scenarios.

- Admin or publishing deal: Songwriters sign administration or publishing agreements with the publishing company, commonly granting 20-50% of publishing income to the publisher in exchange for administration and licensing (low end of the range for admin deal, high end for publishing deal).

- Catalogue ownership: RSVR purchases the publishing rights from the songwriter (or a co-writer) and is thus entitled to ~100% of publishing royalties (potentially less a residual “writer’s share”). Historically, majors didn’t focus on publishing rights; that’s why artists’ rights are sometimes co-owned by smaller publishers (e.g., Chord Music Partners and RSVR, potentially).

In terms of monetization, streaming services pay publishing royalties per stream (mechanical, i.e., for copying the material to its servers or to customer devices… and performance, for communicating it to the public).

Royalties are typically collected through regulated intermediaries (collecting societies, such as GEMA in Germany), regardless of who performs the song. Practically speaking, streaming services thus pay twice for each song: Once for the master recordings and once for the publishing rights.

Collecting societies exist to simplify the administration of publishing rights. Without them, songwriters and composers would have to negotiate directly with every radio station, streaming platform, TV channel, concert venue, or ad agency (which is practically impossible).

However, those societies typically also define the standard fee structure by type of use (e.g., radio, TV, streaming, live concerts, …). In the US, for instance, rates are set and adjusted by the Copyright Royalty Board (CRB) every 5 years. Currently, rights holders receive ~15% of the overall revenue earned from the music.

Publishing revenue is high-margin, recurring, and long-lived, with minimal capital investment once a catalog is established.

Music Publishing revenues are derived from four main sources:

- Digital: the rightsholder receives revenues with respect to musical compositions embodied in recordings distributed in streaming services, download services, and other digital music services;

- Performance: the rightsholder receives revenues if the musical composition is performed publicly through broadcast of music on television, radio, and cable, and in retail locations (e.g., bars and restaurants), live performance at a concert or other venue (e.g., arena concerts and nightclubs), and performance of music in staged theatrical productions;

- Synchronization (“synch”): the rightsholder receives revenues for the right to use the musical composition in combination with visual images, such as in films or television programs, television commercials, and video games;

- Mechanical: the rightsholder receives revenues with respect to musical compositions embodied in recordings sold in any machine-readable format or configuration, such as vinyl, CDs, and DVDs.

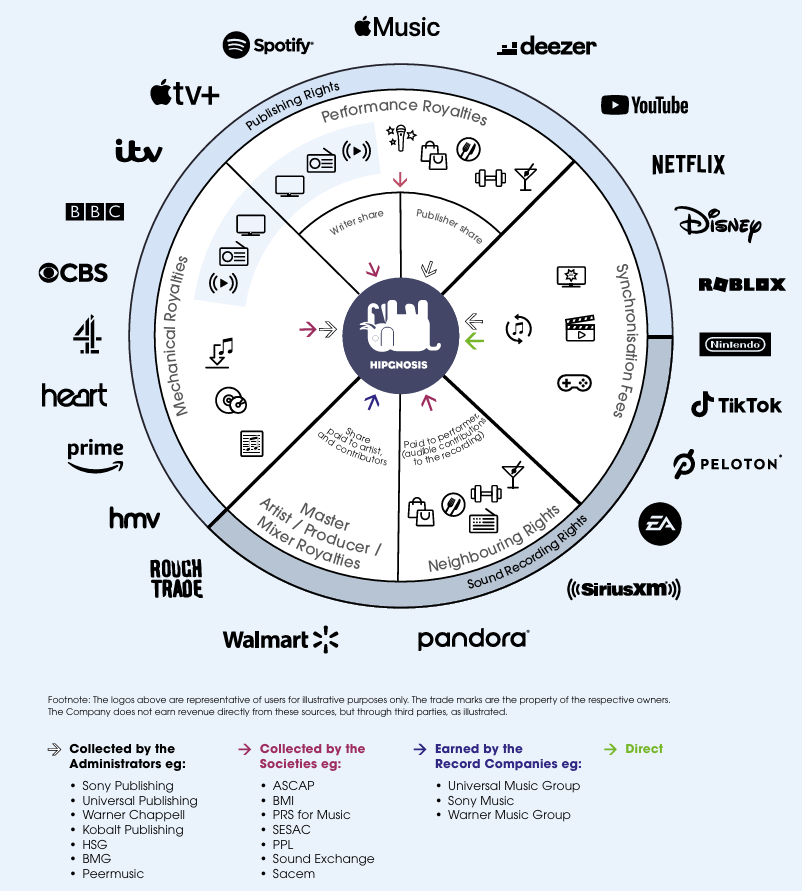

Here’s a pretty good visualization of who collects the revenue in which scenario (courtesy of Hipgnosis Song Fund, 2023):

Figure 6: Sources of revenue in Recorded Music and Music Publishing; Source: Hipgnosis Song Fund annual report 2023

Merchandising

Merchandising earns money by monetising an artist’s brand and fan base through apparel, accessories, and collectibles, often linked to album cycles and tours.

Artists typically retain brand ownership, while UMG provides design, manufacturing, e-commerce, and logistics, earning revenue through revenue sharing or distribution margins.

Merchandise sales are driven by fan engagement rather than streaming volume and therefore diversify artist and label income.

Almost by definition, the margin profile of the merchandising segment is much more similar to that of a retail company (rather than a recording or publishing business).

Merchandising margins vary by distribution channel.

Generally, gross margins are lowest for the music company when they relate to artists’ touring (~8-10%). Products sold through normal retail channels typically have gross margins of ~15%, while DTC revenue (own online shops, e.g., taylorswift.com) earns ~20-25% gross margin.

I’ll just give you the kind of merchandise splits into what I call 3 revenue streams: touring, when you go to see a show. Margins, gross margins, by the way, 8% to 10%. Talent takes all of the money. When it moves towards retail, margins move to the kind of 15% range. And then when you move into direct-to-consumer, you’re up over the 25% kind of margin. – UMG’s COO Boyd Muir at the Morgan Stanley European Technology, Media and Telecom Conference (Nov. 2024)

Regarding DTC: With DTC products (merchandising), music companies are deliberately targeting the ~20% of superfans who are willing to spend ~2-3x as much as a casual music listener.

Products range from coloured vinyl records (about 50% of all vinyl sold is bought for display) to fan shirts to more valuable apparel and even jewellery.

Merchandising is not yet a major business for RSVR, as more attractive growth opportunities are available in the Recorded Music and Music Publishing segments.

Case Study: How to Add Value through Synchronization

As mentioned earlier, synchronization (“synch”) has been one of RSVR’s main growth drivers.

Synch means that teams at publishing companies place music in film, trailers, commercials, etc. The synchronization business represents one of the very few “free-market” parts of the publishing business.

Here, the company can create additional value by actively marketing its rights. This is one of the opportunities that differentiate passive, often PE-owned, royalty funds from small-cap music companies like Reservoir Media, Recognition Music, and majors like UMG.

The following case study illustrates how a strategically placed synchronization (synch) deal can dramatically revive the commercial performance of an older hit song across multiple revenue streams (there are many more examples out there).

Hipgnosis Songs Fund (now Recognition Music), which owns significant master and publishing rights to Journey’s 1983 hit Separate Ways (Worlds Apart), leveraged its relationships with artists and producers to place the song in Netflix’s Stranger Things – Season 4.

A special extended remix was created with Journey’s lead singer Steve Perry and producer Bryce Miller, tailored to the show’s themes. This remix was featured prominently in the official trailer and later within the series itself.

The synch placement had a substantial impact:

- Streaming uplift: Prior to the show, the original song averaged just over 1 million weekly US streams. After the trailer release, streams increased by 68% to 1.82 million per week.

- Revenue growth: Artist royalty income related to the master recording rose nearly 4x compared to pre-2021 levels and more than doubled after the series aired.

- Publishing income: Publishing revenues (notably via co-writer Jonathan Cain’s catalogue) increased significantly across synch, streaming, physical, and performance royalties.

- Physical sales and catalog revival: The remix appeared on the Stranger Things soundtrack vinyl, and Journey’s Frontiers album was remastered and reissued, further boosting sales.

- Cultural spillover: The renewed popularity inspired a cover version by Daughtry in January 2023, sustaining momentum and expanding audience reach.

Overall, total earnings for 2022 increased by 184% year-on-year, demonstrating how a well-executed synch can reinvigorate a legacy song, attract a younger audience, and unlock substantial incremental value across streaming, physical sales, publishing, and performance income.

![Figure 7: Development of weekly streams of Separate Ways (Worlds Apart) [#]; Source: Hipgnosis Songs Fund 10-K 2023](https://montaniumresearch.com/wp-content/uploads/2026/02/RSVR-2-9.png)

Figure 7: Development of weekly streams of Separate Ways (Worlds Apart) [#]; Source: Hipgnosis Songs Fund 10-K 2023

Current Owner Earnings of RSVR

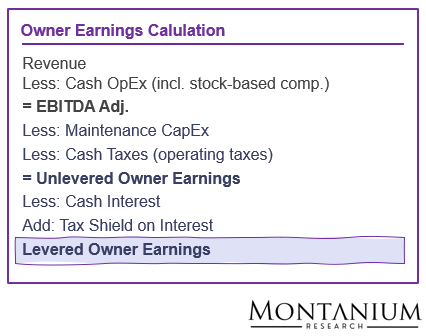

Owner Earnings (according to Warren Buffett) are the sustainable, true cash flows that a business can distribute to its owners without harming its long-term competitive position.

The original definition comes from the 1986 Berkshire Hathaway Shareholder Letter:

Owner earnings represent (a) reported earnings plus (b) depreciation, depletion, amortization, and certain other non-cash charges less (c) the average annual amount of capitalized expenditures for plant and equipment, etc. that the business requires to fully maintain its long-term competitive position and its unit volume. – Warren Buffett, 1986

Short version:

Owner Earnings = Net Income + non-cash charges − Maintenance CapEx

or

In plain English: Levered Owner Earnings represent the cash that actually belongs to the owners, after spending what is necessary to keep the business running at its current level.

Note: We’re taking a long-term perspective here, suggesting that Maintenance CapEx will eventually equal depreciation, resulting in identical tax shields for those items. In reality, Maintenance CapEx, particularly for a high-growth business, will likely be below depreciation expense for quite some time, so with our tax calculation, we typically take a more conservative stance.

Important Accounting Concepts

Reservoir Media reports revenue either on a gross or net basis, depending on whether it acts as a principal or an agent in a transaction:

- If the Company controls the goods or services before they are transferred to the customer, it is acting as a principal and records revenue on a gross basis.

- If the Company does not control the goods or services and merely facilitates the transaction on behalf of another party, it acts as an agent and records revenue net of amounts paid to the other party, reflecting only what it earns for arranging the service.

In the music business, Reservoir usually must pay a portion of its revenues to songwriters or recording artists (known as Royalty Costs). When the Company acts as a principal, it records the full revenue as gross and lists the royalties owed to third parties as expenses.

The resulting number is sometimes called Gross Profit, sometimes Net Revenue or Net Publisher’s Share (NPS) / Net Label Share (NLS).

Operating Returns

As mentioned before, almost 68% of Reservoir’s revenues come from the Music Publishing segment. The Recorded Music segment accounts for ~28%, the „other“ segment, mainly an artist management business, for the remainder.

A closer look at the P&L reveals that there are essentially two major cost items:

- Cost of Goods Sold (making up ~36% of revenue): These costs include royalty costs paid to the artists and songwriters in case Reservoir acts as a principal in terms of revenue recognition, and also amortization of customer advances, as those are recouped by inflowing royalty payments (~USD 22 million in 2025).

- SG&A costs (responsible for ~25% of revenue – same relative size as for the much larger UMG): For the Music Publishing segment, these costs primarily include the costs associated with general overhead (incl. share-based compensation), other administrative expenses, as well as selling and marketing. For Recorded Music, administration expenses also include the costs of promoting and marketing recording artists and music (including costs to produce music videos for promotional purposes and artist tour support).

![Figure 8: P&L Reservoir Media 2025 [USD million]; Source: Reservoir Media annual report 2025](https://montaniumresearch.com/wp-content/uploads/2026/02/RSVR-2-11.png)

Figure 8: P&L Reservoir Media 2025 [USD million]; Source: Reservoir Media annual report 2025

Overall, Reservoir generated operating income (EBIT) of ~EUR 35 million in 2025, corresponding to an attractive margin of ~22%.

As there were basically no one-time effects (restructuring costs and gains/losses from asset sales, etc.), the EBIT to EBITDA Adj. bridge basically looks like this:

![Figure 9: EBITDA Adj. calculation Reservoir Media (2025) [USD million]](https://montaniumresearch.com/wp-content/uploads/2026/02/RSVR-2-12.png)

Figure 9: EBITDA Adj. calculation Reservoir Media (2025) [USD million]

Note that, although we’re interested in looking at “Cash” EBITDA only, we have not added back share-based compensation expense, as, like Warren Buffett, we consider it a real cost to be considered in any Owner Earnings calculation.

Maintenance CapEx

Assessing Maintenance CapEx is one of the key challenges when estimating Owner Earnings.

As a recap: Maintenance CapEx is the investment required to just maintain (not grow) the existing business/profitability level.

Over the past couple of years, Reservoir Media’s investments have varied substantially from year to year, ranging from ~34% to ~181% of revenue (or from USD 50 to USD 196 million in absolute terms):

![Figure 10: Investments Reservoir Media 2022-25 [USD million]; Source: Annual reports](https://montaniumresearch.com/wp-content/uploads/2026/02/RSVR-2-13.png)

Figure 10: Investments Reservoir Media 2022-25 [USD million]; Source: Annual reports

Based on the breakdown in Reservoir’s financials, it is apparent that virtually no capital investment is required to maintain the business at this stage. CapEx is almost entirely used for growth-related investments in and purchases of music catalogs.

As a result, we assumed that Maintenance CapEx represented a very small percentage of total CapEx (1% as a conservative estimate, meaning that Maintenance CapEx as a % of revenue is ~0.6%).

Levered Owner Earnings

As a first step, we calculate unlevered Owner Earnings (UOE) by deducting Maintenance CapEx and Operating Taxes from EBITDA using the above estimation and the standard US Tax Rate of ~21% (which is very close to the reported Tax Rate for fiscal year 2025):

UOE = (USD 61 mn – USD 1 mn) x (1 – 21%) = ~USD 48 mn

Next, we need to consider leverage and interest payments (including the partial tax shield offset).

Without making it too complicated (and ignoring new debt added in FY 2025), at the end of FY 2024, Reservoir Media had ~USD 338 million in interest-bearing debt, on which it paid ~USD 22 million in interest in 2025, equating to an interest rate of ~6.5%.

Thus, current levered Owner Earnings (LOE) are conservatively estimated to be ~USD 30 million:

LOE = UOE – Interest + Tax Shield on Interest = USD 48 mn – USD 22 mn x (1 – 21%) = ~USD 30 million

So basically, if the company were sold today, it would (or should) be priced off this sustainable earnings number available to company owners.

![Figure 11: Current level of Owner Earnings calculation RSVR [USD million]; Source: Own calculations](https://montaniumresearch.com/wp-content/uploads/2026/02/RSVR-2-14.png)

Figure 11: Current level of Owner Earnings calculation RSVR [USD million]; Source: Own calculations

The Value Creation Engine

When assessing a company’s growth mechanics, the key question is not simply how fast revenues or earnings are increasing, but how efficiently incremental capital is deployed.

What ultimately determines the quality and sustainability of growth is the incremental return on invested capital (IROIC or ROIIC) – that is, the return the company earns on each additional USD reinvested into the business.

A high incremental ROIC indicates that growth is value-creating, as each unit of new capital generates disproportionate economic profit, whereas a low incremental ROIC suggests that growth may be dilutive, even if headline growth rates appear attractive.

In this sense, growth only creates shareholder value if it is accompanied by superior returns on incremental invested capital.

In this regard, it is important to distinguish between different sources of growth: structural growth and “capital-driven” growth:

- Structural growth: Growth happening as a result of industry-wide developments or industry structure, in this case, mainly the continued growth of music streaming subscribers and the rise in subscription fees over time, but also the active management of rights with respect to synchronization revenues. These will, by default, likely lead to revenue growth and margin expansion due to the business’s high degree of operating leverage (“economies of scale”).

- Capital-driven growth: Growth happening as a result of dedicated investments, either through the cash flow statement (growth CapEx in the classical sense), or through the P&L (CapEx-like expenses leading to revenue and profit growth down the line). In Reservoir’s case, this mainly involves regularly acquiring music catalogs.

So, how does the “growth engine” look for Reservoir Media?

Structural Growth Opportunity: Sustainable Industry Tailwinds

About 25 years ago, at the end of the last century, the music industry generated most of its revenue from physical products (recorded music only).

Due to digitalization and the introduction of online music access and streaming services, the sale of physical products has been marginalized over time (though vinyl records, in particular, are experiencing a resurgence in popularity at the moment).

Today, streaming revenues represent ~75% of total recorded music revenues. Downloads are slowly disappearing, and physical music sales are pretty much stable.

![Figure 12: Total recorded music revenue by type [EUR billion]; Source: IFPI Global Music Report 2025 | Note: All reporting is translated at average CY 2024 exchange rates. Russia has been excluded from all years.](https://montaniumresearch.com/wp-content/uploads/2026/02/RSVR-2-15.png)

Figure 12: Total recorded music revenue by type [EUR billion]; Source: IFPI Global Music Report 2025 | Note: All reporting is translated at average CY 2024 exchange rates. Russia has been excluded from all years.

Notably, the music industry experienced a major crisis in the 2010s, but somehow survived the illegal download/Napster era.

In terms of consumer behavior, this appears somewhat similar to the developments in the TV/video market (although linear TV at this stage seems much more sticky than music in the early 2010s).

Currently, the “big 4” global streaming services (Spotify, Apple Music, Amazon Music, and YouTube) have ~0.9 billion combined users.

According to UMG’s Capital Markets Day presentation (2024), we’re talking about ~9.5 billion combined accounts if regional streaming services (Deezer, Tencent, NetEase Cloud Music) and social media offerings (Facebook, Instagram, TikTok, WhatsApp, etc.) are included.

There are basically several structural growth drivers in the music industry:

- Continued growth in music streaming (# of subscribers plus pricing)

- Monetization of the so-called “superfans” (which make up ~20% of all music fans)

Streaming

Given the recent developments in streaming platforms and industry dynamics, we conclude that future structural growth will likely be substantial.

Two reasons:

First, streaming platforms currently have ~0.6-0.7 billion paying subscribers. According to Goldman Sachs (“Music in the Air” report), this is likely going to increase to 1.5 billion by 2035 (CAGR ~7-8% pa).

Particularly in the emerging markets, there’s still substantial headroom for streaming services to grow (see graphic below).

Additionally, the production and publication of reels on Social Media platforms are likely to increase substantially, leading to further revenue growth (though this will likely depend on regular renegotiations of blanket deals music companies need to strike individually with companies like Meta).

![Figure 13: Paid subscriber penetration rate by main country [%]; Source: UMG Investor Day Presentation](https://montaniumresearch.com/wp-content/uploads/2026/02/RSVR-2-16.png)

Figure 13: Paid subscriber penetration rate by main country [%]; Source: UMG Investor Day Presentation

Second, prices for streaming offerings, at least in developed markets, can be considered quite low (especially compared to the traditional practice of buying CDs or vinyl and merchandise from favorite artists in retail shops):

- Cost for music per consumption hour is extremely low compared to other media/events (e.g., ~35-1xx USD/hour for a two-hour concert vs. <1 USD/hour for an hour of music streaming).

- Subscribers in emerging markets currently pay substantially less than established market subscribers.

Based on the historical trajectory of price increases for large streaming services (ranging from ~10 to 30% over the past 5 years), we conclude that raising subscription fees could add an additional 2-3% pa to subscription revenue growth.

![Figure 14: Historical price increases of major music streaming services [USD/month]; Source: Websearch](https://montaniumresearch.com/wp-content/uploads/2026/02/RSVR-2-17.png)

Figure 14: Historical price increases of major music streaming services [USD/month]; Source: Websearch

The era of flat subscription fees around 10 USD/month seems to be over, and regular price increases at or above the rate of inflation are expected to be the new norm.

As an add-on, ARPU levels in developing markets will likely converge to Western levels over the medium to long term. (Note: ARPU stands for Average Revenue per User.)

In addition, there seems to be some optimization potential in monetizing ad-supported streams (consisting of ad revenue and subscription fees). As of today, those streaming subscribers typically generate less revenue than premium subscriptions for music companies.

Furthermore, the share of service provider revenue received by publishers has historically moved in only one direction: up!

![Figure 15: Percentage of service provider revenue as defined by CRB [%]; Source: Hipgnosis annual report 2023](https://montaniumresearch.com/wp-content/uploads/2026/02/RSVR-2-18.png)

Figure 15: Percentage of service provider revenue as defined by CRB [%]; Source: Hipgnosis annual report 2023

Although the annual increase has moderated substantially for the period from 2023 to 2027, rates are expected to continue rising (slightly).

Consequently, streaming revenues could rise by approximately 9-11% annually in the foreseeable future, potentially boosting Reservoir Media’s top line by about 5-7% each year (exposure to ~60% of RSVR’s revenue base).

“Superfans”

According to recent market surveys and estimates, so-called “superfans” account for about 20% of all music listeners/subscribers.

The “superfan” has completely different spending patterns compared to the casual music listener. On average, the superfan spends about 3x as much and is particularly interested in owning stuff of his or her favorite artist (i.e., “downloads to own”, physical records, merchandise), plus attends live shows and concerts more frequently.

One sign of superfans’ spending habits is that ~50% of vinyl records sold today are purchased not for listening but as collectibles.

Consequently, music companies, whether independent or collaborating with streaming services, are developing new products aimed at superfans. These new products might include VIP subscription tiers, exclusive live events, and broader DTC offerings on artist websites. At least to some extent, a more “passive” player like RSVR will also benefit from these developments.

Economies of Scale

From a conceptual standpoint, subscriber additions and price increases by music streamers shouldn’t incur any additional overhead costs for RSVR. The same holds true for adding new music catalogs.

Thus, only a minor build-up in overhead costs should be required to administer new music rights (if any). Consequently, the incremental EBITDA margin for any new catalog addition should be approximately equal to gross margin (>60%).

However, at first sight, RSVR’s past revenue growth didn’t yield any benefits from operating leverage as admin costs as a % of revenue virtually stayed flat over the past three years:

![Figure 16: Relative administration costs [% of revenue]; Source: TIKR, company reports](https://montaniumresearch.com/wp-content/uploads/2026/02/RSVR-2-19.png)

Figure 16: Relative administration costs [% of revenue]; Source: TIKR, company reports

At the segment level, though, administrative costs as a % of revenue did in fact decrease for the two main segments, Music Publishing and Recorded Music, since 2023:

![Figure 17: Development of administration expenses on a segment level [% of revenue]; Source: Reservoir Media annual reports](https://montaniumresearch.com/wp-content/uploads/2026/02/RSVR-2-20.png)

Figure 17: Development of administration expenses on a segment level [% of revenue]; Source: Reservoir Media annual reports

The information provided by Reservoir Media in the various annual reports adds additional color. “Negative” changes in administration expenses mainly resulted from:

- An increase in administration expenses in the “Other” segment, which is mainly driven by selling expenses associated with the artist management business (mostly manager compensation) – These costs, which represent ~15% of total admin cost, are likely going to scale with additional segment growth

- An increase in stock-based compensation (from virtually nothing to above USD 4 million in 2025) – this item, ~10% of total admin cost, is likely going to scale with further revenue growth

- Increased regulatory cost related to the IPO in 2021 – this expense is likely not going to move much unless there are going to be additional reporting obligations (management mentions the inclusion of the independent registered public accounting firm’s attestation report on ICFR)

- Cost for establishing the US Recorded Music platform via the acquisition of Chrysalis Records (2019) and Tommy Boy (in 2021) – these were one-off effects, and, based on the earnings call commentary, it seems likely that the established platforms now still have substantial room to grow without adding additional administration layers.

Based on these details, we can subdivide SG&A expenses into two distinct buckets:

- The real administration cost for passively monetizing the master recordings and publishing rights, which, from our understanding, will be more or less fixed for the time being.

- The costs resulting from growing the artist management business and for compensating management (stock-based compensation), which typically scale with revenue growth.

So to conclude: Based on the way the business model works – Spotify, Apple Music, CRB, GEMA, etc., virtually automatically transferring the royalty income to UMG’s accounts (simplifying a bit here) – the capture of further scale benefits in the future seems very likely (but not to be misunderstood here: It’s not a passive business per se but requires regular discussions, negotiations, etc. with DSPs (Digital Service Providers)).

Admin costs basically look like a step-up function: ~25% are completely variable and scale with revenue (stock-based compensation and manager compensation for artist management), and the remainder is fixed until a step-up to the next level is required. Currently, RSVR is building up new growth platforms in the Middle East (PopArabia) and in India (PopIndia).

To remain conservative, in our valuation model, we assumed that ~60% of administration costs scale with revenue and only ~40% are fixed (and benefit from further growth).

Depending on the assumed revenue growth rate, this results in an EBITDA margin expansion of ~250-350 basis points over 5 years.

Capital-driven Growth: Catalog Acquisitions & Consolidation

As stated above, regular acquisitions of music catalogs (e.g., most recently Snoop Dogg and Miles Davis) and record labels (e.g., Tommy Boy) have historically been the main drivers of revenue and profit growth for RSVR.

When publishing rights or record labels/master recordings are sold, value is typically measured as a multiple of the publisher’s/label’s gross margin or net revenue (also called Net Publisher’s Share (NPS) and Net Label Share (NLS), respectively).

Figure 18: Definition of NLS and NPS; Source: Reservoir Media

In the US, transaction multiples have historically been around 15x NPS/NLS; in developing markets (currently particularly South America, the Middle East, and India), multiples range from ~7-9x NPS/NLS.

Over the past decade, Reservoir Media bought music catalogues for ~15.5x NPS/NLS on average. By 2025, the company has been able to reduce this multiple by ~4.4x to ~11.1x today (meaning the company has been able to realize substantial royalty growth over time).

This basically means that such transactions deliver a base yield of ~6.7% unlevered pre-tax (~4.6% unlevered after-tax), before any required step-ups in admin cost are considered, without debt financing, and without accounting for the capture of future growth opportunities.

So today, we’re looking at unlevered catalog economics, which essentially reflect the potential historical earnings that could be achieved with other “real estate-like” asset classes.

Given the typical gross margin of ~60-65%, for each USD of gross profit/NPS/NLS acquired, Reservoir typically acquires a revenue of ~USD 1.55-1.65, which – at 15x NPS/NLS – is equivalent to a revenue multiple of 9-10x or a Sales-to-Capital ratio of ~0.10.

Figure 19: Gross Margin Reservoir Media; Source: Investor presentation

Obviously, acquisition-driven growth will largely depend on the availability of suitable deals.

Based on the latest earnings calls, management seems confident it can continue growing through M&A at a similar pace to its historical performance:

We have an active and robust deal pipeline of over USD 1 billion and look forward to sharing news of our next partnerships with you. – CEO Golnar Khosrowshahi, Q2 2026 earnings call

We are on track with continued M&A for this quarter. And obviously, things are subject to timing and timing shifts, but we anticipate to be continuing at the same clip. – CEO Golnar Khosrowshahi, Q3 2026 earnings call

So assuming that RSVR will find enough attractive deals to reinvest ~75% of revenues (as it did on average over the past 4-5 years) at an average Sales-to-Capital Ratio of ~0.10, the company should be able to grow revenue by ~7-8% pa by M&A activity alone:

Revenue Growth Rate (through M&A) = Reinvestment Rate x Sales-to-Capital Ratio = 75% x ~0.1 = ~7.5% pa

As this calculation is based on an underlying NPS/NLS multiple of ~15x and given that RSVR is increasing its M&A activity in emerging markets at lower acquisition multiples, this growth rate assumption may even be on the conservative side.

For comparison: At a 12x NPS/NLS multiple and similar reinvestment levels, M&A-related revenue could grow by more than 10%.

Putting it all together: Valuation & Intrinsic Value Discussion

To summarize the different growth opportunities:

- Streaming tailwinds could help to grow revenue by a medium to high single-digit percentage amount each year for the foreseeable future (5-7% pa)

- The development of premium products targeting the superfans might lead to another 1-2% pa of revenue growth (only the premium products potentially introduced by the DSPs)

- An additional focus on actively growing synch revenues might add another 1-2% pa

- And finally, continued acquisitions of music catalogs might lead to revenue growth of ~7-10%, depending on the available deals and the concrete acquisition multiples

This means that the overall revenue growth potential could be in the mid- to high-teens range (the simple sum of all identified potentials yields ~14-21% pa).

The upper end of this growth rate range is close to the historical CAGR over the past 6 years.

The lower end aligns more closely with growth rates observed over the past 2-3 years.

Additional factor: Around half of the anticipated growth could be structural, i.e., wouldn’t require any significant capital outlays, meaning that, on a consolidated basis, capital intensity (Sales-to-Capital) would be substantially lower than dictated by successful M&A transactions.

Valuation based on Owner Earnings

To capture the potential outcomes for Owner Earnings 5 years out, we have defined three different scenarios regarding consolidated revenue growth and EBITDA margin expansion:

Figure 20: Main scenario assumptions; Source: Own assumptions

Here’s the rationale: Our “realistic” scenario is anchored in the company’s recent performance, while the optimistic “Blue Sky” scenario projects a growth rate similar to that of the past ~3 years (which remains conservative relative to 2019-22).

The graphic below shows the model results for Owner Earnings growth for the three different scenarios.

Figure 21: RSVR Owner Earnings by YR5; Source: Own calculations

Now, how do we interpret the table?

We observe that levered Owner Earnings would increase to ~USD 63 million in the realistic case, corresponding to a 15.5% IRR over 5 years, assuming the market’s valuation multiple remains largely unchanged. In the optimistic “Blue Sky” scenario, IRR could even increase to ~18%. Even in our conservative “Dark Clouds” scenario, we’d see ~13.5% annual growth in Owner Earnings.

Note: In these scenarios, we didn’t put a ceiling on debt/equity or leverage ratios. Instead, we assumed that any negative Free Cash Flow after reinvestment and dividends (assumed to be zero in this case) would be fully financed with debt.

We then used the resulting debt levels and leverage ratios to cross-check financial stability and balance sheet health.

One key insight we can observe: A substantial share of structural growth would help the company to de-leverage quite quickly (from a Net Debt/EBITDA ratio of above 6x today to a ratio around 4x in 5 years from now), indicating that – from a balance sheet perspective – there would be substantially more room for acquisitions in the coming years… without the need for additional equity injections and assuming that a leverage ratio of 6x EBITDA is sustainable for the company during its current growth phase. From our perspective, leverage would be sustainable given the stable, recurring nature of music royalty cash flows.

Now, what does this all mean for the per-share equity value?

Most importantly, if there are no expectations of change in the (Owner) Earnings multiple, nor any dividend payments or other equity transactions like buybacks or rights issues, then the growth rate in levered Owner Earnings should directly reflect the IRR achievable from this investment.

For RSVR, on a per-share basis, the result can be found in the following table:

Figure 22: Per-share valuation RSVR; Source: Own calculations

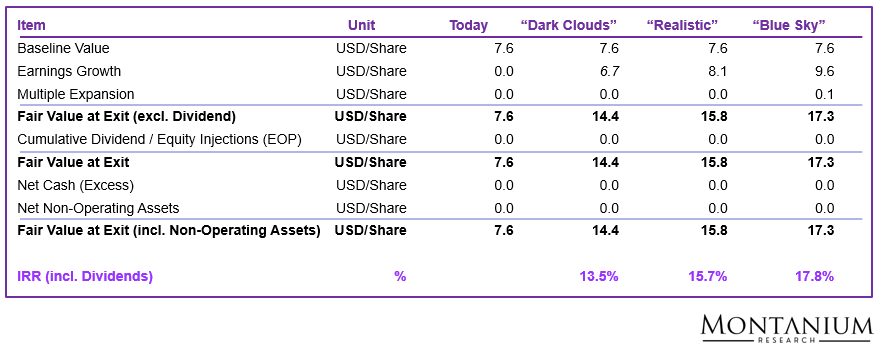

Currently, the RSVR stock is worth ~7.6 USD/share. Based on expected Owner Earnings growth until 2030 (assuming an unchanged earnings multiple) share price would increase to ~15.8 USD/share, representing an absolute return of ~107% or an IRR of ~15.7% over the 5-year period.

Here’s a more visual presentation of the logic:

![Figure 23: Return decomposition RSVR (exit in 5 years) [USD/share]; Source: Own estimations](https://montaniumresearch.com/wp-content/uploads/2026/02/RSVR-2-26.png)

Figure 23: Return decomposition RSVR (exit in 5 years) [USD/share]; Source: Own estimations

Based on our conservative approach, we have not assumed any multiple expansion until the year of exit, meaning the entire return is expected to be driven by earnings growth.

Nevertheless, it seems worthwhile to investigate how a change in the exit multiple would affect the stock’s valuation and expected IRR. As shown in the table below, the IRR increases to above 19% pa if the exit multiple on Owner Earnings (i.e., what the market is willing to pay for each USD of earnings) rises from the current ~16.5x to 19.5x.

![Figure 24: Sensitivity analysis RSVR valuation (IRR) [% pa]; Source: Own calculations](https://montaniumresearch.com/wp-content/uploads/2026/02/RSVR-2-27.png)

Figure 24: Sensitivity analysis RSVR valuation (IRR) [% pa]; Source: Own calculations

After all, even an Owner Earnings multiple of 19.5x corresponds to only ~10x NPS/NLS, positioning our valuation at the very low end of the typical music catalog acquisition multiple range of ~9-15x.

Here’s the calculation logic for the “Realistic” case:

- Based on levered Owner Earnings of USD 63 million by 2030, the equity value would equal ~USD 1,230 million (= USD 63 million x 19.5x)

- Together with a Net Debt of ~USD 440 million in 2030, Enterprise Value (EV) would equal ~USD 1,670 million

- Assuming a relatively stable gross margin of ~64%, gross profit by 2030 (YR5) should be around USD 170 million (= USD 266 mn x 64%)

- Thus, the implied multiple on NPS/NLS would equal ~10x (USD 1,670 million / 170 million).

This immediately raises the question of valuing the business using a typical NPS/NLS transaction multiple. So we also looked at that approach.

Intrinsic Value Assessment based on NPS/NLS Multiples

At a very high level, we can value the company the same way Reservoir Media would value music rights it could purchase: based on a multiple of NPS/NLS or gross margin.

A good reference for the realizable value is Blackstone’s 2024 takeover of the Hipgnosis Song Fund.

Back then, Blackstone paid ~USD 1.57 billion (or ~1.3 USD/share) for the fund, which at that time held around 65,000 songs (including music by Shakira, Ed Sheeran, and Red Hot Chili Peppers, amongst others) and earned a gross profit (Hipgnosis called this “net revenue”) of ~USD 147 million in 2023.

Including another ~USD 500 million of net debt (USD 683 million of debt minus ~USD 183 million of cash and other liquid assets), the NPS/NLS multiple paid by Blackstone for Hipgnosis was ~14x.

Blackstone (BX.N) has agreed to acquire Hipgnosis Songs Fund (SONG.L) for about USD 1.57 billion, trumping an offer from Concord for the music rights owner of artists such as Shakira and Red Hot Chili Peppers, the companies said on Monday.

Blackstone’s formal offer valued the music rights investor at USD 1.30 per share, the companies said, higher than Concord’s USD 1.25 per share offer last Wednesday. – Reuters, April 29, 2024

So, based on this realizable acquisition multiple of ~14x NPS/NLS and given that Reservoir’s gross profit at the end of fiscal year 2025 stood at ~USD 100 million, the company’s music rights today should be worth ~USD 1.4 billion (EV equivalent).

Corrected for a net debt of ~USD 372 million at the end of March 2025, the equity value should be ~USD 1.0 billion, or 15 USD/share, representing a 100% upside to the current share price (or an IRR of ~14.5% over 5 years assuming RSVR doesn’t grow at all going forward).

Of course, in such a “no growth” scenario, it would be most attractive to realize value immediately by selling the company to a larger competitor (likely one of the “Big 3” or a PE royalty fund). Based on several press releases, it seems that Reservoir’s activist shareholder, Irenic Capital, is advocating for exactly this solution.

Looking 5 years out, based on a gross profit of ~USD 170 million, the owned music rights could be worth ~USD 2.4 billion (EV) and ~ USD 2.0 billion (equity value), or 30 USD/share. This would represent an IRR of more than 30% pa over 5 years.

Risks & Threats

While the recorded music business benefits from strong barriers to entry and valuable IP, some market observers see long-term value creation challenged rising artist economics, the bargaining power of streaming platforms, and the strategic uncertainty around AI.

Supplier Power: Rising Cost of Top Talent and Rights

The key structural risk on the supply side is the increasing bargaining power of top artists and rights holders. Creative talent is scarce, and a small number of global superstars capture a disproportionate share of streaming demand. This creates the risk of bidding wars, higher advances, and structurally rising royalty rates to artists, which could compress label margins over time.

In parallel, music catalog prices have increased due to competition from PE and royalty funds. This might inflate acquisition multiples and reduce RSVR’s future returns on invested capital.

While majors still provide critical global distribution, marketing, and infrastructure, the economic rent could gradually shift toward rights owners, especially for top-tier talent.

Buyer Power: Dependence on Streaming Platforms

The major commercial risk on the demand side is the industry’s structural dependence on a small number of dominant streaming platforms (Spotify, Apple Music, Amazon Music, YouTube, Tencent, etc.).

These platforms control consumer access and discovery via algorithms and playlists, giving them meaningful leverage in licensing negotiations. Since end-user switching costs are low and content offerings are similar, platforms are under constant pressure to optimize pricing and margins, which may cap long-term revenue share for royalty owners.

However, as streaming platforms cannot realistically exclude the Big 3 catalogs, the relationship seems to be in a healthy balance.

Substitutes: The AI Risk

The most important long-term existential risk is the potential substitution of human-generated music by AI-generated content.

So far, most realistic use cases for AI (background music, deepfakes, AI-assisted creation) do not materially threaten the core economics of the majors. For instance, AI-generated songs already account for 30-40% of all songs available on Spotify, yet they generate only ~0.5% of revenues.

The key uncertainty is whether fully AI-generated artists or virtual bands could achieve mass emotional relevance and compete with human stars at scale, without the support of the relationships and reach of a record label.

As Bill Ackman puts it:

If you think about it, there’s lots of other technologies and computers that have been used to generate music over time but no one falls in love with a computer generated track. And Taylor Swift, incredible music, but it’s also about the artist and her story and her physical presence and the live experience. […] So I think AI is really going to be a tool to make artists better artists. – Bill Ackman (Pershing Square) on the Lex Friedman Podcast

The industry’s response suggests that AI is being treated less as a threat and more as a new monetization layer, with majors recently shifting from litigation to licensed partnerships.

Still, AI remains the biggest strategic uncertainty regarding the long-term scarcity value of music IP, and managing fake tracks and licensing music snippets, sounds, melodies, etc. to AI is a key issue for streaming and music companies to address.

Overall, compared to the music piracy of the 2000s and 2010s, this sounds like a manageable task.

Regulation and M&A Constraints

Regulation is not a fundamental operational risk, but it limits external growth via M&A. Given the majors’ already high market shares, large acquisitions are increasingly subject to antitrust scrutiny, especially in the EU and the US.

This creates a structural ceiling on inorganic growth, forcing majors to rely more on organic monetization of existing catalogs rather than on industry consolidation.

However, RSVR should still be some orders of magnitude away from such constraints.

Conclusion, Catalysts & Portfolio Decision

Based on current industry tailwinds (7%+ structural growth), prior experience with acquiring music catalogs, and the substantial gap between current valuation and realized transaction multiples (~8x vs. 14x NPS/NLS), we believe a double-digit return over the next 3-5 years is entirely possible.

During that timeframe, a potential catalyst could be a takeover offer from either a strategic buyer (a larger competitor like UMG, WMG, or Sony) or a PE fund aiming to further consolidate the market.

Apart from that, we believe that the continued growth of royalty income will, by itself, lead to a rising share price. Management around Golnar Khosrowshahi has a ~15-year track record of building and growing the company at attractive rates (with sufficient skin in the game and a long-term mindset).

Threats from AI seem unjustified given the proprietary nature of master recordings and publishing rights. Negotiating licensing fees for using song snippets, text passages, etc., in AI productions just seems to be the next step in the music industry’s “monetization” journey of the past decade. In the end, it takes a lot o

However, for the optimistic scenario to materialize (return >20% pa), a couple of things need to go right in the medium-term future:

- Growth of streaming platforms needs to materialize; the DSPs need to introduce a differentiated product offering (addressing the “superfan” demand), and continue raising prices regularly (ideally above inflation rate)

- Attractively priced M&A deals need to be available for the foreseeable future

- RSVR’s team needs to continue adding value to the portfolio through landing movie, TV, commercial, gaming, etc. placements (see the “synch” growth case study above)

We’d thus be willing to allocate 5-10% of our total portfolio assets to music royalties and believe RSVR is one of the best opportunities currently available. At ~7.6 USD/share, the stock looks promising.

To enter the position, we first allocate ~50% of the target 5%.