Table of Contents

- Sidebar: Why Airlines Lease Part of their Fleet

- Background and Business Model of Air Lease

- Capital Market View of Air Lease

- Investment Thesis

- Conclusion

- Disclaimer

- Disclosure

The business model of leasing aircraft to large airlines has been discussed in several places recently. Among others, Woodlock House wrote about Air Lease, and David Einhorn and Horos Asset Management wrote about AerCap. Reason enough for me to take a closer look at the aircraft leasing business for MONTANIUM Research.

A small side note on my own behalf: Incidentally, it took me quite a bit of effort to present an idea here that is not “unique” and that several investors have already reported on elsewhere. As a blogger, I naturally want to offer my readers content that is as original as possible. As an investor, however, I don’t want to limit myself and exclude good ideas just because they have already been considered by others. With this in mind, I hope that my article will still contain some new insights for those who are already familiar with Air Lease.

Sidebar: Why Airlines Lease Part of their Fleet

The proportion of the total aircraft fleet that is leased now stands at around 40% worldwide (up from around 25% in 2000 and around 2% in 1980). Airlines lease part of their fleet for various reasons:

- They need less cash and do not have to worry about down payments and financing for the aircraft.

- Airlines can breathe easier when it comes to fleet size. Leasing allows them to flexibly adapt their fleet to competition, market conditions, etc.

- Airlines can add new aircraft to their portfolio at an earlier stage because leasing companies typically have better delivery positions due to their size (Air Lease currently represents approximately 14% of Airbus and Boeing’s order books, making it one of the largest – if not the largest – single customer).

- The airline does not need to bear the residual value risk because it can return the aircraft to the lessor at the end of the lease agreement.

- Airlines can deploy leased aircraft fairly quickly, even in special situations, and thus maintain their flight schedules. This applies, for example, to the current case of the Boeing 737 MAX 8, which is currently grounded.

For these reasons, passenger aircraft leasing will continue to play an important role in the aircraft market in the future.

Background and Business Model of Air Lease

The business model of Air Lease, founded in 2010, is not so different from that of a real estate company such as Vonovia or DEFAMA, except that the assets rented (or leased) are movable property.

Air Lease purchases aircraft on favorable terms from the major aircraft manufacturers Airbus and Boeing and then leases them on a long-term basis to over 90 airlines from more than 50 countries. The leases are largely “triple net leases,” in which the airline pays not only the lease rate but also all operating costs, including maintenance costs. This means that Air Lease has nothing to do with the operational running of the aircraft.

Cash flows are fairly stable and predictable due to long-term leases. Air Lease focuses on young and modern aircraft, which are generally held in the portfolio for the first third of their useful life (i.e., until they are approximately 8-10 years old). The fleet, which mainly consists of the most widely used and therefore most liquid “single aisle” aircraft, is therefore just under 4 years old on average.

In terms of capital investment or the net book value of the aircraft (this refers to the average book value, i.e., the mean of the book value at the beginning and end of the year), leasing revenues are quite stable at around 11.5% and thus largely independent of global macroeconomic cycles. The average remaining lease term of the Air Lease portfolio is currently around 7 years.

On the cost side, there are really only three main blocks:

- Interest payments: The average interest rate is currently around 3%, including risk premium. More than 80% of the debt has a fixed interest rate, and around 90% of the loans are unsecured, i.e., they are granted solely on the basis of the credit rating and do not require a specific aircraft as collateral.

- Depreciation: The depreciation period of 25 years (assuming a residual value of 15%) is slightly below the actual useful life of 30 to 40 years per aircraft, which tends to result in lower net profit but also in hidden reserves.

- Central costs: At approximately 6.0% of revenue, sales and administrative costs are low compared to the competition. In addition, clear economies of scale are evident (in 2012, SG&A costs still amounted to 8.7% of revenue).

Figure 1: Air Lease SG&A costs as a percentage of revenue [%], source: Air Lease annual reports

Approximately 70-80% of investments in new aircraft are made with debt capital, so that the debt/equity ratio is usually somewhere between 2.5 and 3.0. If necessary, parts of the investments are financed by opportunistic asset sales… or must be financed by asset sales in order to comply with the limits regarding the D/E ratio.

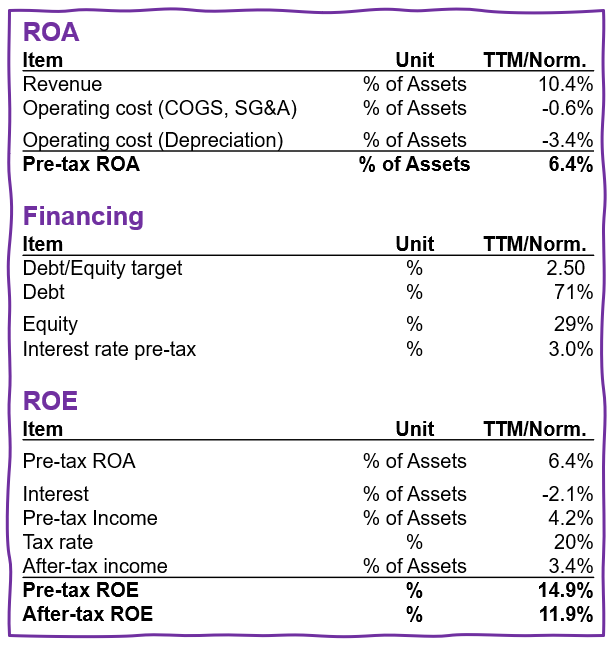

Overall, these characteristics result in a business model with a return on equity (ROE) after taxes of approximately 12%, as you can see from the following table:

Figure 2: Economics Air Lease (derivation return on equity)

As you can see, the return on total capital is still quite modest and only becomes very attractive due to the leverage effect, i.e., the use of approximately 70% debt capital. The same applies for Free Cash Flow (FCF). Due to the high CapEx requirements in the growth phase, FCF (before taking net new debt into account) is initially negative.

In such business models, the debt ratio (D/E ratio) is also typically the factor limiting growth. Regular capital increases can accelerate growth accordingly if there are appropriate opportunities in the market. However, as far as I know, Air Lease has not made use of this option since its IPO in 2011.

Over time, this results in the following fundamental internal value drivers for Air Lease’s business model:

- Revenue growth through the purchase of additional aircraft and leasing them to airlines

- Improved credit rating and thus reduction of the risk premium on the base interest rate as the company grows

- Largest order book among the major OEMs and thus the potential to negotiate (even) better purchasing terms and delivery positions with Airbus and Boeing

- Leveraging economies of scale with regard to central and SG&A costs

Air Lease continues to be led by a highly experienced management team. Both the current CEO, John L. Plueger, and the Chairman of the Board of Directors, Steven F. Udvar-Hazy, bring several decades of experience in the aircraft leasing business to the table. Udvar-Hazy co-founded ILFC (International Lease Finance Corp.) in 1973 and was also its CEO until 2010. ILFC was one of the first aircraft leasing companies ever and a precursor to Air Lease’s competitor AerCap.

Capital Market View of Air Lease

The current macroeconomic risks – the trade dispute, the fragile economy in China, the impending Brexit, the resurgent crisis in Italy, etc. – are fueling market participants’ fears of declining passenger numbers and further airline bankruptcies. Following the insolvency of Air Berlin in 2017, several other airlines went bankrupt worldwide, including Germania, Small Planet, Jet Airways, Avianca Brazil, etc. (a more comprehensive list can be found here, for example). Increasing airline insolvencies can, of course, lead to corresponding payment defaults on the part of leasing companies and, in some cases, even to problems with the return or repossession of aircraft.

In addition, rising interest rates in the US are causing additional uncertainty regarding the (re)financing costs of leasing companies. As already briefly mentioned, high debt is a core component of the business model and therefore the dependence on the interest rate environment is quite high. More on the risks involved below.

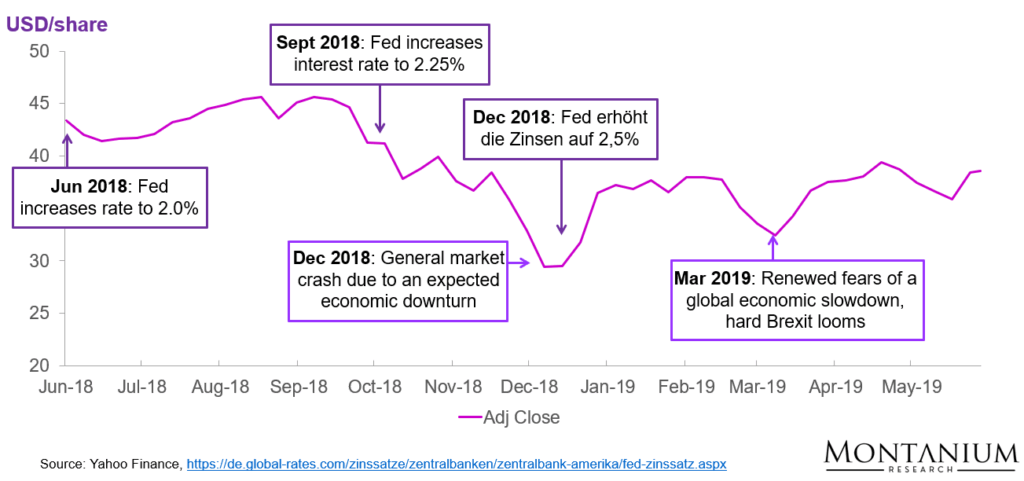

Figure 3: Air Lease share price performance; Source: Yahoo Finance

However, Air Lease’s current share price of around USD 38 per share is still significantly above its recent low of around USD 28. A further strengthening of negative sentiment could therefore push the price down a little further.

Investment Thesis

Future Value Drivers

Air Lease’s planned growth is based on the assumptions that (1) air traffic and demand for aircraft will continue to increase in the coming years and decades, and that (2) the proportion of leased aircraft in total air traffic and/or Air Lease’s share of the leasing market will also continue to grow. These assumptions are based on several overarching trends:

- An ever-growing middle class, especially in developing countries

- A partial shift away from the “hub and spoke” concept toward more direct city-to-city routes (including long-haul)

- The increasing obsolescence of the existing aircraft fleet and the resulting significant need for renewal

- Continued high demands on the flexibility and cost efficiency of airlines

- The size of the leasing companies’ order books in conjunction with long delivery times and order backlogs for the most important aircraft types

I believe it is quite undisputed that air traffic will continue to increase over the next few years for the reasons mentioned above. Basically, more and more people will be able to afford to fly (despite presumably higher prices due to rising environmental standards). In addition, almost half of the current aircraft fleet will have to be replaced over the next 20 years.

Aircraft manufacturers have also recognized the trend toward more direct flights and thus smaller aircraft. At the Paris Air Show, Airbus recently unveiled its A321 XLR, a modified A321 that is also suitable for long-haul flights thanks to an additional fuel tank. As with many other Airbus aircraft, Air Lease is once again the “launch customer,” i.e., one of the first customers for the aircraft.

Figure 4: Key growth drivers Aircraft leasing; source: Air Lease investor presentations

Due to their financial position and situation, as well as the long delivery times for new aircraft, airlines will continue to have to rely on leasing companies. Even if they finance the new aircraft themselves, many airlines will be dependent on leasing companies, at least temporarily, due to delivery times.

This is partly due to the high competitive pressure on airlines and the resulting strong focus on cost efficiency. WizzAir, for example, a local low-cost airline focusing on Eastern Europe and also a customer of Air Lease, estimates that the renewal of its fleet (from the A321 CEO to the A321 NEO) will reduce operating costs by up to 20%. This is where Air Lease’s fleet and delivery positions offer major advantages over the competition (AerCap, etc.), but also over the options available to many airlines:

Figure 5: Average age and cost per flight hour of Air Lease fleet; Source: Aero Analysis

Air Lease’s order pipeline at Airbus and Boeing currently comprises approximately 360 aircraft, most of which are scheduled for delivery within the next five years (i.e., by approximately 2023). Just recently, Air Lease also ordered 21 of the new Airbus A321 XLR long-haul aircraft for delivery from 2023 at the Paris Air Show.

According to statements made by the CEO in the last earnings call, approximately USD 5.8 billion is to be invested in 2019, with approximately USD 3.5 billion to be financed by new debt, USD 1 billion from the sale of used aircraft, and the remainder from operating cash flow. This represents a completely different order of magnitude compared to previous years, as a maximum of USD 3.5-3.8 billion has been invested in new aircraft in a single year to date (depending on whether interior fittings are included or not).

Leasing agreements with various airlines already exist for the majority of the new aircraft, but these will only come into effect once the aircraft have actually been delivered. This means that the current delivery bottlenecks at Airbus and Boeing should not lead to any recourse claims on the part of the airlines against Air Lease.

Here is a timeline of the planned deliveries to Air Lease by Airbus and Boeing (the current order with Airbus is not yet included):

Figure 6: Planned aircraft deliveries to Air Lease [# aircraft], source: Air Lease investor presentation

Over the next five years, an average of approximately 70 aircraft per year are scheduled for delivery. With a current aircraft fleet of 275 aircraft (end of fiscal year 2018), this represents substantial growth. However, delays are expected for both Airbus and Boeing in 2019 and 2020 as a result of bottlenecks in the supply chain and the delivery freeze on the 737 MAX 8. Just for comparison: competitor AerCap has approximately 1,400 aircraft in its fleet, making it significantly larger.

In addition, I believe that the debt ratio and the covenants under the loan agreements are currently limiting the upside growth rate.

Without a capital increase (which is not unusual for such business models) and with a debt/equity target of 250%, revenue growth of approximately 15% per year should be possible. In order to prevent debt from rising too high and at the same time be able to pay for the aircraft ordered, some used aircraft with current leasing contracts must always be sold, which naturally slows down revenue growth somewhat. In principle, however, it should be entirely possible to temporarily exceed the target debt/equity ratio of 2.5 without encountering any problems with the covenants (statement from a recent conference call).

Valuation and Return Potential

The expected return on an investment in any stock consists mainly of three components:

- Dividends or regular distributions

- Multiple expansion if the share price is undervalued compared to the current enterprise value

- Future growth in earnings or cash flows

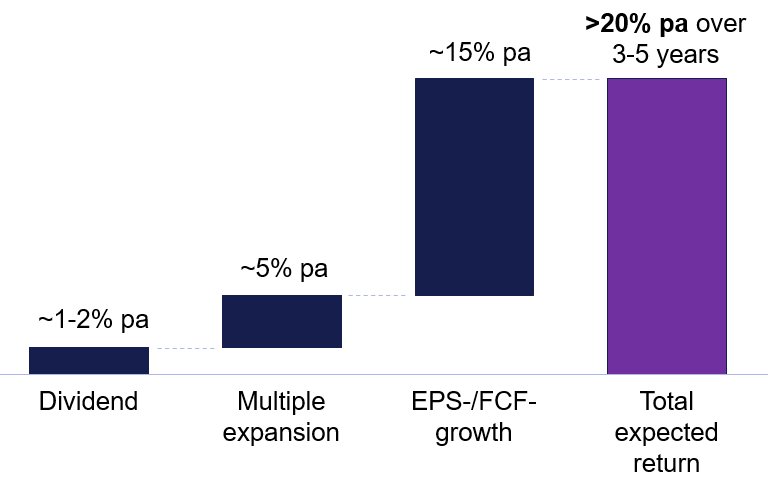

For Air Lease, I see potential of >20% per year for the next few years, driven mainly by further growth in top line and thus net earnings per share (EPS) and operating cash flow:

Figure 7: Decomposition of expected return; Source: Own estimations

As you can see, dividends and the recovery from the current undervaluation also play a certain role. However, compared to profit growth, these two return components tend to take a back seat.

Dividend and Multiple Expansion

Air Lease’s dividend yield is very modest, and according to management’s plans, most of the operating cash flow will continue to be used for investments in additional aircraft. I assume that a distribution in the range of 10% of net profit will continue to be made in the future.

The recovery in the value of the share (based on the current P/E ratio of ~8) could amount to approximately 5% per year. Based on a conservative estimate of a long-term growth rate of 1.5% for the years 6ff, the fair P/E ratio should be somewhere in the range of 10 to 12 (however, despite attractive growth prospects, the historical average over the last 8 years was only around 11.5). Incidentally, I am looking at the expected long-term growth because I want to consider the growth component separately and not count it twice as part of the P/E ratio.

Figure 8: Historical P/E and P/B ratios of Air Lease; Sources: Morningstar, Alpha Vantage

Since aircraft leasing is a very asset-intensive business model, I also looked at the ratio between the share price and book value (P/B ratio). Air Lease shares are currently trading below book value (P/B ratio ~0.9), historically at around 1.2 times. Incidentally, Air Lease’s assets consist almost exclusively of aircraft.

There are no significant intangible assets and no goodwill from any company acquisitions. This means that the tangible book value—i.e., the book value adjusted for intangible assets—and the book value are virtually identical. In addition, as already indicated above, depreciation is relatively aggressive, which should lead to hidden reserves, albeit on a relatively small scale.

Earnings Growth

In my view, the largest contribution to returns over the next few years will come from further growth in earnings and (operating) cash flow.

Based on the approximately 360 aircraft already ordered for delivery over the next five years and the target debt ratio of 250%, I consider revenue growth of approximately 14-15% per year to be realistic. By way of comparison, if growth were to occur more or less as per the order book without any limit on the debt ratio, my calculations suggest that we would already be looking at revenue growth of around 18-20% per year (naturally with a corresponding negative effect on the average age of the fleet, because in such a scenario virtually no used aircraft would be sold).

I do not foresee any major changes in the EBITDA margin and depreciation rate for the time being. However, an improvement in interest coverage could lead to a slight improvement in the credit rating and thus the risk premium on the base interest rate. Given the high relevance of interest expenses in the income statement, this could contribute to additional growth in the profit margin of approximately 1-2%.

On the other hand, the regular issuance of stock options and new shares will probably lead to a partial dilution of EPS growth. Based on the historical development of outstanding shares, I expect a negative effect of approximately 0.5%.

Taking all effects into account, I consider EPS growth of around 15% to be entirely realistic for the coming years.

Here are my key assumptions for the valuation in detail:

- Limitation of the debt ratio or debt/equity ratio to 250% and thus partial limitation of new net debt (i.e., either postponement of orders into the future or increasing asset sales to finance all ordered aircraft… the latter more likely due to the business model)

- Constant risk-free base interest rate over the next few years

- After 5 years, the target size (“steady state”) is reached and the strategy is adjusted towards “cashing out.” This essentially means no further investments in further growth

- No additional economies of scale on the SG&A side (however, Air Lease sees further positive effects here in the coming years)

All in all, I consider the assumptions to be quite conservative. On the one hand, the expected growth could well result in economies of scale on the SG&A side. On the other hand, with the debt ratio capped at 250% after 5 years, the company’s growth will probably not be complete and steady state will not yet have been reached, as can be seen from the latest orders in Paris and the relative size of its competitors.

Opportunities and Risks

The following risk factors are typically cited in relation to the “aircraft leasing” business model:

- Problems with refinancing or passing on interest rate changes (especially increases, of course) to airlines via the leasing rate

- Insolvencies of airlines and thus default on lease payments or problems in placing Air Lease aircraft on the market

- Further delivery delays at OEMs (Airbus, Boeing) or engine manufacturers (currently Rolls Royce in particular is experiencing problems), resulting in longer-term delays in growth

On the opportunities side, I see above all the realization of further economies of scale in terms of sales and administrative costs. While these are certainly possible, the effect on the EBITDA margin should not exceed approximately 1% (Air Lease is already the benchmark compared to its competitors).

Let’s take a closer look at the two main risk factors.

Rising Interest Rates

An environment of rising interest rates can have a significant negative impact on Air Lease’s financing costs and thus also on its earnings. However, in my view, there are several reasons that currently argue against a stronger effect in this regard.

First, the probability of a pause in the interest rate hikes initiated in the US is increasing due to the current global economic slowdown. In fact, Air Lease even expects average interest costs to improve over the coming years, as some expensive loan agreements from the past are likely to be refinanced at more favorable terms.

In addition, Air Lease has a fairly balanced credit maturity profile, meaning that only a small portion of its debt will need to be refinanced in each of the coming years:

![Air Lease loan maturity profile [USD million], Source: Air Lease Q1 2019 quarterly report](https://montaniumresearch.com/wp-content/uploads/2025/11/image11.png)

Figure 9: Air Lease loan maturity profile [USD million], Source: Air Lease Q1 2019 quarterly report

In conference calls, management also regularly points out the possibility of passing on interest rate increases to airlines. If necessary, these would take place with a slight delay at most. Of course, the terms of loan agreements on the one hand and leasing agreements on the other do not always run 100% synchronously (i.e., they are usually not renegotiated at the same time).

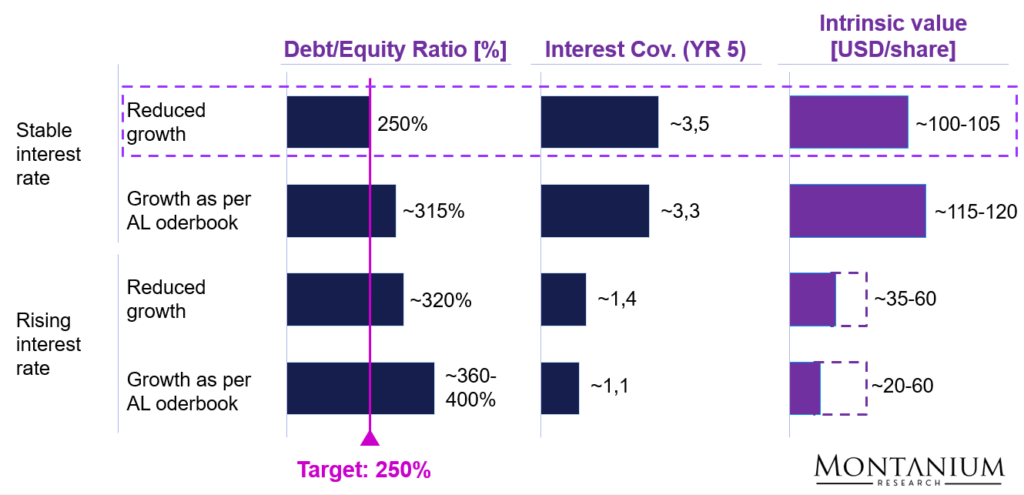

However, in order to understand the effects of interest rate increases (without the possibility of passing them on to airlines) on the valuation of Air Lease, I looked at a few scenarios. As you can see from the following chart, an increase in the base interest rate in the market (assumption here +1.5%) would have a massive impact:

Figure 10: Different valuation scenarios depending on interest rate and FCF growth

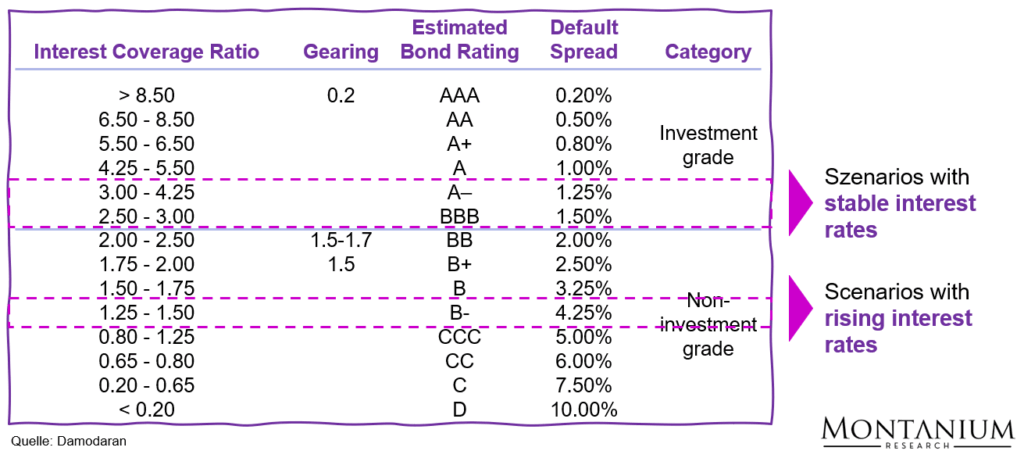

An increase in the risk-free base rate should initially lead to a deterioration in interest coverage, which in turn could cause banks to significantly increase the risk premium (default spread) to be paid.

Here is a typical relationship between interest coverage, bond rating, and default spread (for more details, read the article How we calculate the cost of debt):

Figure 11: Impact of interest rate scenarios on credit rating; Source: Damodaran, own estimations

Incidentally, the assumption here is that all banks would unanimously demand an interest rate increase for their loans at the same time and would not be willing to negotiate loan terms, etc. In this respect, the scenario may be somewhat pessimistic, but in my view it illustrates the downside risk of this investment quite well.

Airline Bankruptcies

Overall, airlines are in a much better position today than they were a few years ago. Many sustainably unprofitable players have disappeared from the market and markets have consolidated further. In certain regional markets, quasi-monopoly structures can now be found. Lufthansa, for example, now has a 98% market share in domestic flights in Germany, while Air France KLM dominates the French market in the same way.

As can be seen from industry-wide EBIT margins, the global airline industry has been profitable for almost 10 years now. Although margins have deteriorated somewhat since 2016, they are still above the levels seen in the years 2011 to 2013. For your information: The major wave of bankruptcies and consolidation in the US airline industry in response to the global financial crisis of 2008-09 largely took place before 2011.

![EBIT margin of the global airline industry [%]; Source: Statista](https://montaniumresearch.com/wp-content/uploads/2025/11/image14-1024x421.png)

Figure 12: EBIT margin of the global airline industry [%]; Source: Statista

Nevertheless, airlines have repeatedly gone bankrupt over the last 10 years (Air Berlin, Germania, etc.). However, this has usually only led to the disappearance of the company, not to the mothballing of the respective aircraft – Lufthansa, for example, simply took over a large part of Air Berlin’s aircraft (as many as were permitted under competition law).

If you believe in the long-term trend of passenger growth and at the same time look at the order backlogs at the OEMs, then I think you can assume with a certain degree of certainty that a new owner will also be found for the aircraft of a bankrupt airline.

Air Lease has also lost only two aircraft over the last eight years, which speaks for the quality of the screening process for potential customers. CEO John Plueger regularly points this out in conference calls.

Conclusion

Air Lease leases aircraft to over 90 airlines worldwide and collects a regular leasing fee for this. Operating costs, maintenance, etc. are covered by the airlines, so Air Lease is not involved in the operational running of the aircraft (“triple net lease”). The company currently has approximately 280 aircraft in its portfolio, with more than 360 additional aircraft on order from the major OEMs Airbus and Boeing.

The business model is relatively stable and generates a return on equity after taxes of approximately 12%. In addition to depreciation on the investment, namely the aircraft, the largest cost factors can be considered to be interest payments on loans and the company’s sales and administrative costs.

Due to various factors, it is advantageous for many airlines to lease at least a certain portion of their fleet from companies such as Air Lease. The proportion of leased aircraft in the total global aircraft fleet has grown to approximately 40% in recent years. Further growth in passenger numbers and the increasing age of the fleet should continue to make leasing an attractive business model in the future.

The biggest risk factors are interest rate increases and payment defaults/losses of aircraft as a result of airline insolvencies. However, these risks appear to be limited in the coming years.

All in all, I believe that Air Lease shares offer a potential return of approximately 20% per annum over the next 3-5 years.

Disclaimer

This document is provided for informational and educational purposes only and does not constitute investment advice, a recommendation, or a solicitation to buy or sell any security or financial instrument. All information, opinions, estimates, and forecasts contained herein reflect the judgment of the author as of the date of publication and are subject to change without notice.

While every effort has been made to ensure the accuracy and completeness of the information, no representation or warranty, express or implied, is made regarding its fairness, accuracy, or completeness. The author and associated entities may have positions in, or may from time to time buy or sell, the securities or financial instruments discussed in this report. Investing in financial instruments involves risks, including the possible loss of principal. Readers should conduct their own independent research and analysis and seek professional advice before making any investment decisions.

Disclosure

The author of this report, Montanium Research, certifies that the views expressed herein accurately reflect their personal views about the securities and issuers discussed. The author has not been compensated by any company or issuer mentioned in this report for preparing or publishing this content.

As of the date of publication, the author does hold a position in the securities mentioned in this report. This disclosure is provided in the interest of full transparency.